How does health insurance work?

by Kaiser Permanente | October 6, 2025

Health insurance can feel confusing. Whether you’ve started a new job, moved to a new city, or it’s just time to pick a plan — it can feel like a lot to sort through. If so, you’re not alone: about half of people surveyed say they don’t fully understand their coverage, and one-third aren’t sure what costs their plan covers.1

So how does health insurance work? When you buy a health plan, you pay a monthly cost called a premium. Then, the plan helps pay for covered care — from preventive visits and prescriptions to tests, hospital care, and emergencies.

Choosing the right coverage matters. This guide explains plan types, what’s covered, and costs — plus clear steps to choose and use a plan that fits your budget. With this information, you’ll feel more confident when you compare options.

Why do I need health insurance?

If you’re generally healthy, you may wonder whether you really need coverage. Health insurance helps you:

- Protect your budget. A broken wrist or appendix surgery can cost thousands of dollars. With a plan, you pay your share up to your out-of-pocket maximum — and the plan pays the rest.

- Use preventive care. Many preventive services are covered at no additional cost when you see doctors in the network — things like annual checkups, vaccines, and screening tests.

- Get care faster. A primary care doctor helps you navigate your care, from same-day advice to referrals.

- Access tools and perks. Many plans include virtual care, wellness programs, and fitness discounts that can help you stay on track.

No matter what stage of life you’re in, coverage matters — it helps you avoid large bills and makes preventive care easier. Learn more about health insurance for young adults.

What does health insurance cover?

Most health insurance plans help pay for preventive care that helps you stay healthy and catch issues early. They also pay for medical care like doctor visits, tests, hospital care, and emergency care. Coverage and costs can vary by plan and location, so always check your plan documents for details.

How do different health plans work?

Health plans differ in how you get care, what rules you follow, and how you share costs with the insurance company. The plan you choose can affect your monthly costs, which doctors you can see, and whether you need referrals for certain services.

Some common plan types are:

- Health maintenance organization (HMO): Care from doctors and hospitals that work with your plan. Usually, you choose a primary care doctor, and referrals are often needed to see a specialist. In most cases, emergency care is covered even if you have to go outside your plan.

- Preferred provider organization (PPO): More flexibility to see specialists without referrals. You can also see doctors who don’t work with your plan, but you’ll usually pay more. In most cases, emergency care is covered even if you have to go outside your plan.

- Exclusive provider organization (EPO): Care from doctors and hospitals that work with your plan. Referrals are often not needed.

- Point of service (POS): A mix of HMO and PPO features.

Learn about HMO and PPO plans and how they compare. You can also read about health insurance types to understand all your options.

Coverage levels — the 4 metal tiers

What are metal tiers?

The 4 metal tiers are coverage levels that are usually used for health insurance marketplace plans. They show how you and the plan split average costs. They aren’t plan types and don’t measure quality of care.

How do the tiers compare?

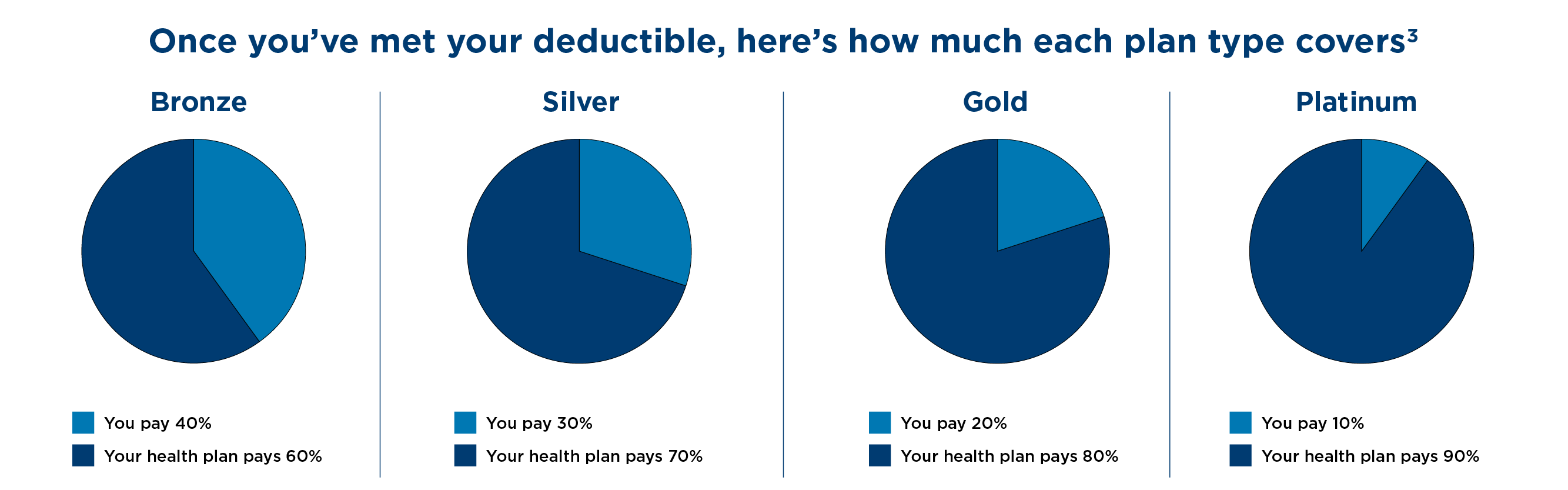

Once you’ve met your deductible, here’s how much each coverage level pays.2 The higher the monthly premium, the more the plan pays when you get care.

- Bronze plans usually have the lowest monthly premiums, the highest deductibles, and the highest out-of-pocket costs. You pay 40% and the plan pays 60%.

- Silver plans have moderate monthly premiums, deductibles, and out-of-pocket costs. You pay 30% and the plan pays 70%.

- Gold plans come with higher monthly premiums but lower deductibles and lower costs when you get care. You pay 20% and the plan pays 80%.

- Platinum plans have the highest monthly premiums but the lowest deductibles and the lowest costs when you get care. You pay 10% and the plan pays 90%.

How do health plan costs work?

Knowing the main types of health plan costs can help you budget and plan for care.

- A premium is what you pay each month to keep coverage.

- A deductible is what you pay for covered care before your plan pays more.

- A copay is a set dollar amount you pay for a covered service or medication.

- Coinsurance is your share of the cost for a covered service, usually a percentage.

- Your out-of-pocket maximum is the most you’ll pay in a year for covered care. After you reach it, your plan pays 100% of most covered services.

Example: If a lab test is $100 under your plan:

- Before you meet your deductible: You pay the full $100 — unless your plan covers that service without the deductible.

- After you meet your deductible: If your coinsurance is 20%, you pay $20, and your plan pays $80.

How can I set a healthcare budget

- Start with your premiums. Multiply your monthly premium by 12.

- Add likely care. Think about routine visits, prescriptions, or therapy. Learn the difference between the types of doctor visit costs.

- Plan for surprises. Set aside money for unexpected care, such as a broken bone, a visit to the emergency room, or an unplanned surgery. Put it toward your deductible and your share of the cost.

- Use tax-advantaged accounts. Learn about using a flexible spending account (FSA) or health savings account (HSA) to help cover some of your costs.

- Check your plan’s documents for exact costs and coverage.

What’s the difference between getting in-network versus out-of-network care?

Every plan has a network of doctors, labs, hospitals, and other providers it works with. You usually pay less when you choose an in-network doctor or facility. Some plans ask you to choose a primary care doctor and get a referral before you see a specialist.

If you get out-of-network care — except in emergencies — you may pay more, or your plan may not cover the cost.

Learn more about getting in-network versus out-of-network care.

What do I need to know about referrals and prior authorization?

- Referrals connect you to specialty care when your plan requires a primary care doctor to coordinate care.

- Prior authorization means your plan reviews certain services before you get them to confirm coverage.

Your plan documents explain when these steps are needed and how they work.

When and how can I get health coverage?

You can sign up for coverage during open enrollment, which happens once a year. If you have a qualifying life event — like losing coverage, moving, getting married, having a baby, or turning 26 and moving off a parent’s plan — you may be able to enroll during a special enrollment period.

Some ways people get coverage include:

- Through work — Your employer may offer several plan options.

- On your own — Individuals and families can shop plans and choose one that fits best.

- Public programs — Depending on your income and household size, you may qualify for Medicaid or the Children’s Health Insurance Program (CHIP). These accept applications year-round.

- Between jobs — You may be able to pay the full premium to keep your last job’s plan for a limited time through COBRA while you compare other options.

How do I choose a health insurance plan?

Picking a plan can feel like a lot — almost 3 out of 4 insured adults worry about affording health care, including out-of-pocket costs and prescriptions.3

Factors to help you decide on a health plan

- Budget — Set your budget and look at the premium and what you’ll pay when you get care.

- Doctors and facilities — Check that your doctors, labs, and hospitals are in the network.

- Medications — Look up your medications in the plan’s formulary (list of covered drugs).

- Convenience — See what options for virtual care and tools are available.

- Life changes — If you expect a move, a new job, or to have a baby, consider plan flexibility and costs.

Which coverage level should I choose?

- Bronze plans are a good fit for people who rarely need care and want a lower monthly bill. Premiums are lower, but costs are higher when you do get care.

- Silver plans work well for people who want balance — moderate monthly premiums and moderate costs at the visit.

- Gold and Platinum plans might be the right choice for people who use care more often or want more predictable costs. You’ll pay more each month but less when you get care.

- High deductible plans with an HSA can help people who want to save pre-tax dollars and set aside money for future health costs.

If you’re choosing through work

Use the information in this article when looking at your options. Learn more about what questions to ask your employer about coverage.

How do I use my health plan?

Once you’re enrolled, you can make the most of your coverage by using your plan’s online tools, choosing the right providers, and knowing where to go for care.

- Choose a primary care doctor if your plan requires one.

- Use your plan’s website or app to schedule visits, refill prescriptions, and get virtual care.

- Know where to go. Choose primary care for routine needs, urgent care for conditions that aren't an emergency but require medical attention soon, and the emergency room for conditions that require medical attention right away to prevent serious harm to your health.

- Review your Explanation of Benefits after a visit to see how your plan covered the service — it’s not a bill.

Understanding your plan documents

- Summary of Benefits and Coverage gives an overview of coverage and common costs.

- Evidence of Coverage explains benefits, limits, exclusions, referrals, and authorizations.

- Formulary lists covered drugs and any steps like step-therapy requirements — which are rules that ask you to try a lower-cost medicine first — or prior authorization.

Learn more about how to read your plan documents.

Pharmacy basics

- Generic and brand-name medications. Generics usually cost less and work the same way as brand-name drugs your plan covers.

- Tiers. Plans may group drugs into tiers with different copays or coinsurance.

- Ways to fill. You may be able to use mail-order or an in-network retail pharmacy.

Perks that may come with your plan

Many plans also include extra perks, like convenient ways to get care in person or online, self-care and mental health apps, healthy lifestyle programs, and fitness discounts.

Does preventive care cost me anything?

Many preventive services are covered at no extra cost when you see doctors in the network. Your plan documents list what’s included.

Do deductibles reset?

Most plans reset their deductibles each plan year. Check your plan’s start date and whether separate deductibles apply for medical care and prescriptions.

What if I have 2 health plans?

If you’re covered under 2 plans (for example, your own plan and a parent’s plan), one plan pays first and the other may pay some of the remainder. This is called coordination of benefits. Your plan documents explain how it works.

What should I do if something looks off?

Your Explanation of Benefits shows the cost of your visit, what your plan paid, and what you may still need to pay. If something looks wrong, contact your plan or the provider’s billing office with your Explanation of Benefits and bill handy. Your plan documents will explain how to appeal a coverage decision.

Learn more about Kaiser Permanente

Ready to see your options? You can view plans, find doctors and locations, and get to know our uniquely designed care model.

Footnotes

1Larry Levitt, MPP, and Drew Altman, PhD, “Complexity in the US Health Care System is the Enemy of Access and Affordability,” JAMA Network, October 26, 2023.

2“How to Pick a Health Insurance Plan,” Healthcare.gov, April 1, 2024, healthcare.gov/choose-a-plan/plans-categories

3Lunna Lopes et al., “Americans’ Challenges with Health Care Costs,” KFF, March 1, 2024.