-

Health insurance works by helping you pay for medical care and services, so you don’t have to pay all your health care costs on your own.

The best health plan for you is one that meets your health care needs, budget, and expectations. But it can be tough to know what to look for — and what to avoid.

Before you decide on a plan, you’ll need to think about:

- Your health and how often you need care

- How much coverage you need

- How much money you’re willing to spend

- How different health plans work

- What each plan offers beyond the basics

Understanding your total health care costs is key to getting the most out of your plan and avoiding potentially expensive surprises.

How to find a health plan that’s right for you

Not sure where to start?

If you don’t know an HMO from an HSA, you’re not alone. But rest assured – we’re here to make health care easier to understand.

Compare plans & choose

We have a variety of health plan options to fit your needs and budget. All of them offer the same quality care, but the way they split the costs is different.

Apply online

Once you pick your plan, fill out the application online to become a member and experience what it means to thrive.

Common questions to help you get started

-

We offer a variety of plans to help fit your needs and budget. All of them offer the same quality care, but the way they split the costs is different. Not all of these plans are available in all states.

Copay plans: Copay plans are the simplest. There is no deductible and you pay for care according to an easy-to-follow copay or coinsurance schedule. Your monthly premium is higher, but you’ll pay much less when you get care.

Deductible plans: With a deductible plan, your monthly premium is lower, but you’ll need to pay the full charges for most covered services until you reach a set amount known as your deductible. Then you’ll start paying less – a copay or coinsurance. Depending on your plan, some services, like office visits or prescriptions, may be available at a copay or coinsurance before you reach your deductible.

Virtual plans: Virtual plans are a type of deductible plan that have lower costs for preventive and primary care when the visits are via telehealth (virtual visits) versus in-person visits. With a Virtual plan, you have several ways to access high-quality care — for many health conditions — that’s both affordable and convenient. You’ll get to choose how you get care, by taking full advantage of our many no-cost virtual care options — while having access to in-person primary care whenever you need it.

HSA qualified plans: HSA-qualified deductible plans are deductible plans with a special feature. With this plan, you can set up a health savings account (HSA) to pay for health costs like copays, coinsurance, and deductible payments. And you won’t pay Federal income taxes on the money in this account. You can use your HSA anytime to pay for care, including some services that may not be covered by your plan, such as eyeglasses or adult dental. And if you have money left in your HSA at the end of the year, it will roll over for you to use the next year.

Catastrophic plans: These plans are available in some markets for people under age 30, and those over 30 with a hardship exemption. They have very high deductibles and low monthly premiums, and cover limited preventive benefits before the deductible. They might be a reasonable strategy to safeguard yourself against the worst-case events, such as becoming very ill or hurt. However, until the plan's yearly deductible is met, you are responsible for paying for most medical costs.

-

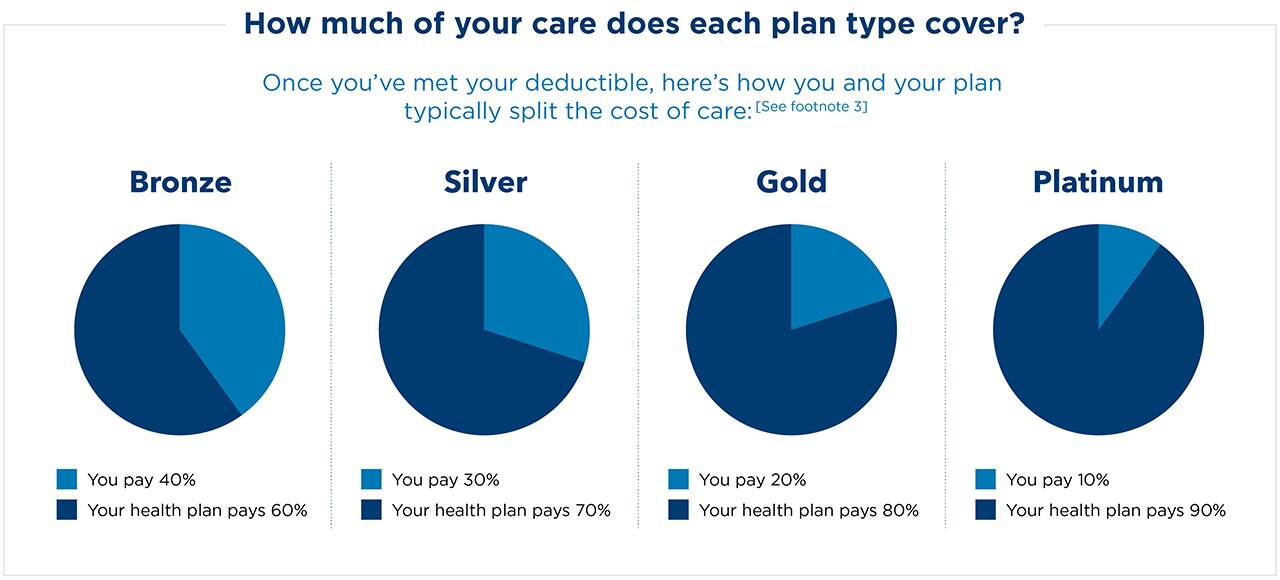

Individual and Family Plans are organized into 4 coverage levels — also called metal tiers — getting to know them will help you understand what you are responsible for paying and which plan will best fit your health care needs.

It is important to understand that the metal tiers only reflect the difference in cost sharing, not the types of care we provide. You receive the same high quality Kaiser Permanente care in all of our plans.

Bronze ($): Lowest monthly premium | Highest deductible | Highest out-of-pocket costs for care

A good choice for healthy people who rarely see the doctor and want a low-cost way to protect themselves in case they occasionally get injured or sick.Silver ($$): Moderate monthly premium | Moderate deductible | Moderate out-of-pocket costs for care

A good choice for generally healthy people willing to pay a little more each month to have fewer out-of-pocket expenses before your health plan starts covering the cost of care.Gold ($$$): Higher monthly premium | Lower deductible | Lower out-of-pocket costs for care

A good choice for people with dependents and who use health care services regularly throughout the year.Platinum ($$$$): Highest monthly premium | Lowest deductible | Lowest out-of-pocket costs for care

A good choice for people with known health issues who have frequent specialty care needs, tests, and prescriptions.

Footnotes

3. “The ‘Metal’ Categories: Bronze, Silver, Gold & Platinum,” HealthCare.gov, accessed September 14, 2021.

-

Healthcare costs can be overwhelming for many individuals and families. The Affordable Care Act (ACA) makes it easier for individuals to compare a variety of health insurance plans and select the one that best suits their needs and budget. The ACA also provides financial assistance (sometimes referred to as subsidies) to qualified individuals based on income.

For general income guidelines and to see if you qualify for federal or state financial help, start a quote. You can also compare plans, calculate your rate, and apply for health plans.

Learn about Individual and family health plan affordability

-

Getting you connected with a doctor who suits your individual needs is our top priority. We know how important it is to find a doctor who's right for you. When you have a doctor you connect with, it’s easier to stay healthy.

To choose or change doctors at any time, for any reason, browse our online profiles by region.

Find top-notch doctors, specialists, and pharmacies near you

-

In general, you can only change or apply for health care coverage during the yearly open enrollment period (OEP). But if you have a qualifying life event, you may be able to change or apply for coverage for a limited time (the special enrollment period).

Generally, a special enrollment period (SEP) lasts 60 days after the triggering event occurs. That means if you've experienced a qualifying life event, you have 60 days from the day of the qualifying life event to change or apply for health care coverage for yourself and/or your dependent. In some situations, if you are aware that you will lose coverage or your eligibility for coverage will change in the future, you may be able to apply for new coverage 60 days before the loss of coverage.

Examples of qualifying life events are:

- Loss of minimum essential health coverage

- Gaining, becoming, or losing a dependent or death of a subscriber or a dependent

- Permanent relocation with access to new plans

- Change in income changing your eligibility for federal assistance

- Changes in employer health coverage making you eligible for a premium tax credit

Learn more about qualifying for a special enrollment period in your state

-

Health care is full of industry-speak. Without knowing the basics, it’s hard to understand how things work. Look up the key terms you need to know as you navigate the world of health care.

Get informed, stay connected

Discover the many ways that Kaiser Permanente supports your health.

Get the full story on health coverage at Kaiser Permanente

Article

Health plan costs - what to know

This 4-part series covers health plan costs, including setting a budget, tips for saving money, and understanding medical care costs.

Article

What is Kaiser Permanente?

We offer care and coverage together to support your total health — and simplify your entire health care experience.

In California, KFHP medical plans are offered and underwritten by Kaiser Foundation Health Plan, Inc., One Kaiser Plaza, Oakland, CA 94612 • In Colorado, all medical plans are offered and underwritten by Kaiser Foundation Health Plan of Colorado, 10350 E. Dakota Ave., Denver, CO 80247 • In Georgia, all medical plans are offered and underwritten by Kaiser Foundation Health Plan of Georgia, Inc., Nine Piedmont Center, 3495 Piedmont Rd. NE, Atlanta, GA 30305 • In Hawaii, all medical plans are offered and underwritten by Kaiser Foundation Health Plan, Inc., 711 Kapiolani Blvd., Honolulu, HI 96813 • In Oregon and southwest Washington (Clark and Cowlitz counties), all medical plans are offered and underwritten by Kaiser Foundation Health Plan of the Northwest, 500 NE Multnomah St., Suite 100, Portland, OR 97232 • In Washington (except Clark, Cowlitz, and certain other counties), all medical plans are offered and underwritten by Kaiser Foundation Health Plan of Washington, 2715 Naches Ave. SW, Renton, WA 98057 • In Maryland, Virginia, and the District of Columbia, all medical plans are offered and underwritten by Kaiser Foundation Health Plan of the Mid-Atlantic States, Inc., 2101 E. Jefferson St., Rockville, MD 20852