When comparing different types of health insurance, you want a plan that lets you see the doctors or specialists you need. You also want one that works for your budget. The most common choice you’ll have is between a health maintenance organization (HMO) and a preferred provider organization (PPO) plan. These options work differently and have different health plan costs you should know about.

The differences between an HMO and a PPO

In this article, you’ll learn about:

- How HMO vs. PPO plans work

- HMO vs. PPO plan costs

- HMO vs. PPO advantages and disadvantages

- Other types of health plans

- What to consider when choosing a health plan

How HMO plans work?

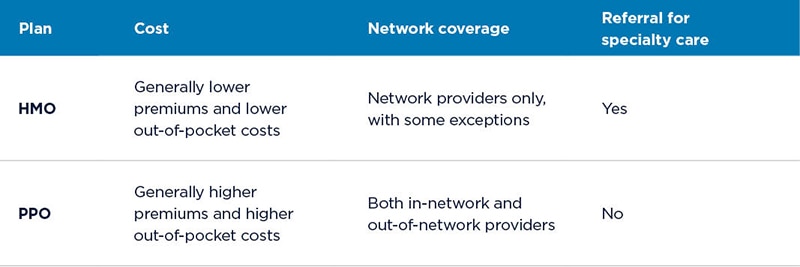

First of all, what is an HMO? An HMO is a defined network of health care providers that contracts with a health plan to provide care at preapproved rates. Your personal doctor manages your care and refers you to specialists in the network.

You’ll mostly get care from doctors, nurses, and specialists in the network. But HMO plans sometimes refer members to specialists outside the network when they need specific services. HMO plans also cover medical emergencies. This lets members get care from any emergency room.

Do HMO plans require referrals?

In most cases, you’ll need a referral from a personal doctor to get specialty care. But certain specialty services — like ob-gyn and optometry — may be available without a referral.

The costs of an HMO plan

HMO plans coordinate care for a set payment. That means you typically have:

- Lower monthly premiums (the amount you pay each month for coverage)

- Lower deductibles, or no deductibles (the amount you need to pay before your plan starts contributing to your medical bills)

- Lower payments for covered services

Remember: If you get nonemergency care from an out-of-network provider, you’ll pay the full cost.

How do PPO plans work?

With a PPO plan, you can see any doctor you want — inside or outside the network. Your PPO plan will have a network of preferred providers. It will probably cost you less money to see them. But you still have the option to see doctors outside that group.

Do PPO plans require referrals?

No. You can get specialty care without a referral from a personal doctor — from both in-network and out-of-network providers.

The costs of a PPO plan

PPO plans often have higher monthly premiums and out-of-pocket costs than HMO plans. You may also need to pay a deductible before your benefits begin. If you see an out-of-network doctor, you’ll usually have to pay the full cost of your visit and then file a claim to get money back from your plan.

Which is better — an HMO or a PPO?

It depends on what’s important to you. The best health plan is the one that meets your needs. If you like lower costs and think coordinated care makes things easier, an HMO plan might be a good choice. If you want to continue seeing a doctor or specialist who isn’t in a plan’s HMO network, think about a PPO plan.

Advantages and disadvantages of HMO plans

Advantages

- You pay lower monthly premiums and usually lower out-of-pocket costs, including prescriptions.

- When you get care in the network, you have fewer claims to file.

- Your personal doctor coordinates your care. This can make it easier to take care of your health.

Disadvantages

- HMO plans require you to stay inside their network for care, unless it’s a medical emergency.

- If your current doctor isn’t part of the HMO’s network, you’ll need to choose a new personal doctor.

Advantages and disadvantages of PPO plans

Advantages

- You can see providers both inside and outside the network.

- You can visit specialists without a referral, including specialists outside the network.

Disadvantages

- You typically pay higher monthly premiums and costs for care than with HMO plans.

- You have more responsibility for managing and coordinating your care.

Other types of health plans

HMO and PPO plans are the most common health plans. But there are other plan types you should know about.

Exclusive provider organization (EPO) plans

An EPO plan is somewhere between an HMO and PPO in terms of flexibility and cost. You don’t need a referral to see a specialist, but there aren’t any out-of-network benefits.

Point-of-service (POS) plans

A POS plan also combines different parts of HMO and PPO plans. With a POS plan, you usually need a referral from a personal doctor to see a specialist. You can also see out-of-network health care providers — but at a higher cost.

What to consider when choosing a health plan

Before choosing a plan, think about your health care and budget needs. Do you want a personal doctor to coordinate your care? Do you want lower out-of-pocket costs and fewer claims? Do you need health insurance for young adults? Are there specific wellness perks you want included? Once you know the answers to questions like these, you can review the information above and start making your decision.

If you get health coverage through your employer, also consider these questions to ask your employer as you compare plans. And if you have questions about your options, talk to your human resources representative. They should have health plan documents that show the benefits of each plan they offer. This can help you choose the best one for you and your health.